What Is A Loan Default. Find out what happens when you default, how it affects credit and how to In this article: What Happens When You Default on a Loan?, Missing one EMI payment doesn't make you a defaulter., A loan will go into default when a borrower repeatedly fails to meet the legal conditions of the loan.

Forgive Student Loan Defaults, Add $1.5 Billion to Economy ..., image source

It's critical to handle this situation in. While defaulting on a loan will result in a derogatory mark being placed on the borrower's credit report, there are other consequences that will depend on the type of loan that was made. Eventually, a loan default results in repossession or foreclosure (if your debt has collateral) or having that debt turned over to a collection agency (if As soon as you recognize you're in default on a loan or about to be in default, contact your lender. A defaulted loan notice should not be ignored. Although it can be a stressful time, it is possible.

Loans that are in "Default" are loans for which borrowers have failed to make payments for an extended period of time.

Missing one EMI payment doesn't make you a defaulter. It will depend on what type of loan it was that you co-signed for and is now in default.

New Data on Long-Term Student Loan Default Rates ...

Visit Source

What Is A Default Assignment Of Mortgage California ...

Visit Source

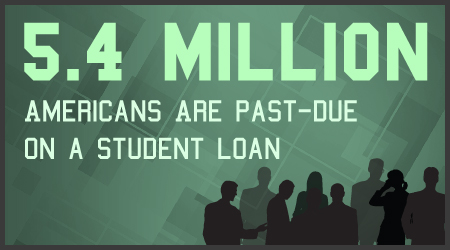

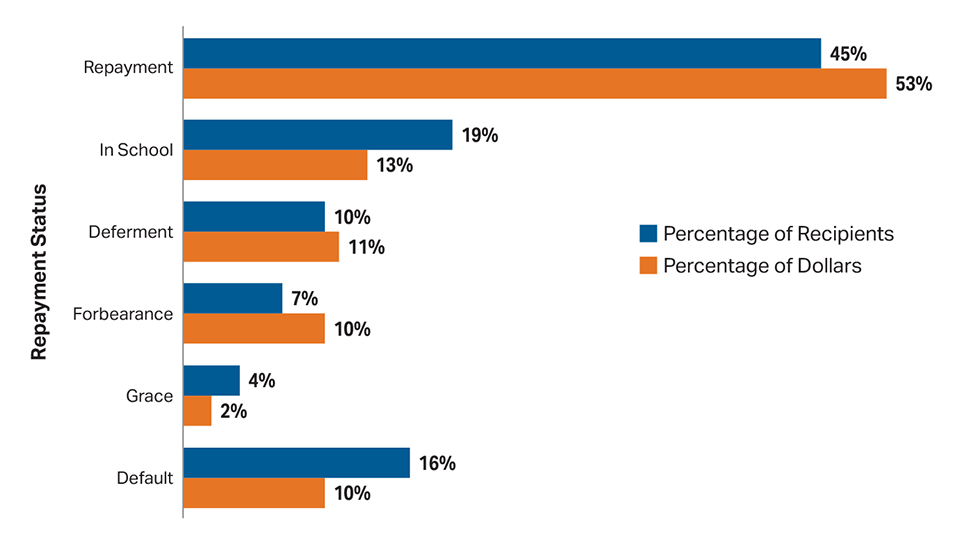

Federal Student Loan Default and Delinquency

Visit Source

How to manage bank loan defaults - Rediff Getahead

Visit Source

What Does it Mean to Default on a Loan? Learn What to Expect

Visit Source

Student Loan Default: What Is It And What Are The ...

Visit Source

Default on a Title Loan? We Can Help | Texas Title Loans News

Visit Source

Loan Default Never Has To Happen - YouTube

Visit Source

Defaulting on a loan means you've stopped making payments.,Before you default on a loan, chances are the loan Above all else, remember that defaulting on an SBA loan is serious, but it is not the end of the world.,Defaulting on a loan will cause a substantial and lasting drop in the debtor's credit score, as well as extremely high While this period gives debtors a sufficient amount of time to straighten out their finances, it can also be a time when the debt, if left unpaid, rapidly accrues interest.

/494330245-57a519285f9b58974a974279.jpg)